Summary: This article examines the increasing use of Application Programming Interfaces (“APIs”) in the insurance sector and their role in enabling embedded and digital distribution models. It discusses how API platforms are integrated for distribution of insurance products with third-party digital platforms, offering coverage at the point of transaction. The article also highlights the key legal and operational considerations arising from such arrangements and outlines the regulatory framework under the Insurance Act, 1938.

Have you noticed how, when you’re checking out on a merchant platform these days, you’re often presented with an option to add insurance for your purchase? And just like that, within seconds, a policy is issued in your name! In this article, we will examine what happens in those few seconds, as an Application Programming Interface (“API”) comes into the picture to give the customer a seamless experience of purchasing insurance as an “add-on”. With digital journeys becoming the norm, insurers are leveraging APIs to convert digital consumers into policyholders. And as the industry undergoes this quiet transformation, we examine a host of legal and regulatory issues and how to navigate them, at the convergence of digitalisation, embedded finance, and evolving customer expectations.

API Integration

An API is a software intermediary that enables two applications to communicate and share data. At its core, it is a set of protocols that allow different software systems to exchange information seamlessly. In simpler terms, APIs serve as a bridge between different digital systems, enabling data exchange. In the insurance industry, this means that an insurer’s back-end system can seamlessly connect with a third-party platform (such as a fintech app, e-commerce website, or mobile platform) to deliver a digital insurance experience.

From a consumer’s perspective, the role of APIs is often invisible. However, in the background, APIs transmit a bundle of data to the insurer’s system. Details typically include the customer’s name, contact details, the item or trip details, along with the premium amount and a transaction reference. These are processed in the insurer’s system, which produces a quote. Upon acceptance, the insurer generates the policy or coverage certificate and transmits it to the customer.

Since the experience resembles a single, seamless purchase, it is easy to assume that the merchant platform is the insurance provider and it will handle all aspects of the insurance transaction. However, regulatorily, the insurance contract remains with the insurer, and the entity responsible for the sale in regulatory terms is the regulated entity.

The Regulatory Landscape

Indian insurance law does not regulate “APIs” as a technology layer. Instead, it regulates subjects such as (a) who can solicit/ procure insurance, (b) the conduct expected at solicitation and sale, (c) remuneration connected with procuring business, and (d) operational controls around customer data, outsourcing-like arrangements, and cyber security.

Protection of policyholders under PPHI Regulations

The IRDAI (Protection of Policyholder’s Interests, operations and allied matters of insurers) Regulations, 2024 (“PPHI Regulations”) provides severalnorms for policyholder protection, advertisements, premium receipt, disclosures, proposal records, grievance redressal, allied operational requirements, etc. Accordingly, an API-enabled journey must be designed such that regulatory compliance is maintained, irrespective of the interface through which the customer transacts.

Cyber security considerations

Cyber security expectations apply to the insurer, under the Information and Cyber Security Guidelines, 2023, irrespective of which platform user interface is the front-end. The insurer remains responsible for cybersecurity and outsourcing standards, including encryption, authentication, rate limiting, and incident response protocols.

Remuneration

Remuneration structures must be evaluated considering statutory prohibitions on commission and rebate practices. Arrangements involving rebate, commission, rewards, remuneration, etc., should be evaluated through the legal lens of the Insurance Act’s prohibition on paying for soliciting/ procuring business.

Multi-level marketing

Multi-level marketing is prohibited under Section 42A of the Insurance Act, 1938. In the context of API-enabled distribution, any delegation of functions by an insurance intermediary can be challenging and hence must be assessed from the perspective of the relevant applicable regulations. Any API infrastructure established between any platform and an insurance intermediary requires a more cautious approach, as insurance intermediaries face additional restrictions on delegation of functions and multi-level marketing arrangements.

Licensing and solicitation under Insurance Act

Section 40(1) of the Insurance Act restricts paying any remuneration or reward to persons who are insurance agents or intermediaries/ insurance intermediaries “for soliciting or procuring insurance business”. It is the statutory guardrail that should be considered on how unlicensed platforms may participate in an insurance sales journey (including where that participation is technologically enabled through APIs).

Key Considerations

Whilst API-driven distribution models present significant advantages, they also bring a distinct set of regulatory and operational considerations.

| Issue | Key Challenges | Safeguard Measures |

| Disclosures and Consent | Embedded distribution models raise concerns around customer awareness. Where policies are bundled into broader service journeys, customers may inadvertently purchase insurance without understanding the key terms, exclusions, or claims process, or without awareness that the insurance policy is being directly distributed via the insurer-owned API. | Insurers and platforms should ensure that disclosures are clear and accessible, in line with regulatory expectations on transparency and informed consent. |

| Commission and Remuneration | Remuneration arrangements with entities unregistered with IRDAI present a risk, as remuneration based on a share of commission received from a policy may be characterised as impermissible. | Remuneration structures should be carefully evaluated in light of statutory prohibitions on commission and rebate practices. |

| Cybersecurity and Data Integrity | APIs, by their nature, expose digital endpoints that can be exploited if not properly secured. Vulnerabilities such as unauthorised access, data scraping, or fraudulent API calls can result in large-scale breaches. | Insurers should ensure that robust cybersecurity measures for all integrated APIs are implemented. |

| Licensing and Solicitation | A primary concern is identifying which party (whether the insurer or the host platform integrating the insurer-owned API) is responsible for specific customer-facing actions such as solicitation, disclosures, and policy servicing. | Third-party platforms (e.g., e-commerce apps or fintech providers) that are not licensed to sell or solicit insurance products should ensure that the act of solicitation remains with the insurer, and that adequate consent and notice mechanisms are in place when redirecting users to the insurer’s authorised interface. |

Conclusion

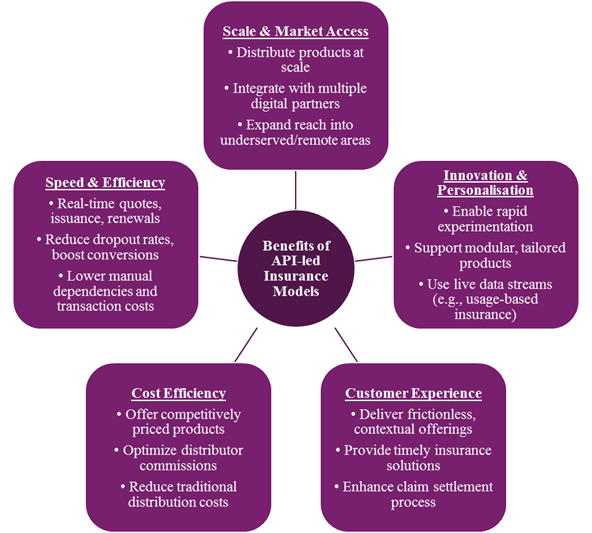

APIs serve as powerful enablers of insurance distribution, supporting real-time sales, deeper digital partnerships, and innovative coverage models. However, the regulatory expectations are evolving in parallel. Third-party platforms, insurers, and insurance intermediaries must carefully assess their roles, interfaces, and data practices before launching API-led journeys. Whether structured as an embedded offering or a front-end sales flow, legal clarity on solicitation boundaries, disclosures, marketing and advertising practices and remuneration arrangements will determine the long-term viability of such models.

As India’s digital economy continues to expand, API-led insurance distribution will play an increasingly central role in making protection accessible, affordable, and contextually relevant. Success will depend on striking the right balance between innovation and compliance, ensuring that convenience never comes at the cost of consumer protection or regulatory integrity.